The recession that isn’t happening: don’t underestimate the growth potential of the US economy

Prof. Dr. Jan Viebig Global Co-CIO ODDO BHF

When the Covid pandemic shut down the global economy in Spring 2020, it ended the longest expansion phase in US history, which lasted 42 quarters. For more than ten years, there had been repeated warnings that the next recession was imminent. But the US economy remained on a growth trajectory. Despite a few weak quarters and even a few with negative growth (Q1 2011, Q1 2014), the US economy grew by an average of 2,5% per year between mid-2009 and the end of 2019. Only the outbreak of the coronavirus pandemic – an external shock – could end this long-lasting expansion.

For several months now, experts and market participants have been discussing the risk of a recession in the US again. Some observers, including well-known institutions, have upgraded the risk of recession. The regular Bloomberg surveys among experts indicate a median probability of 30%. The New York Fed’s estimation model, which is based on the steepness of the yield curve, goes as far as to indicate a recession probability of almost 60% over a 12-month horizon. And the so-called Sahm Rule, which is derived from the rise in the unemployment rate, triggered a recession alert in July 2024.

However, we believe that the risk of a ‘real’ recession in the US is low. Real in this case means that there is a significant contraction in economic activity in the US as defined by the National Bureau of Economic Research. The US economy is broadly diversified, less dependent on international influences than the European economy for instance, and highly innovative. In addition, potential growth (ie. the growth opportunities with full utilization of production capacities) is significantly higher than in Europe at 2 to 2.5%, so that the ‘normal’ distance from the null line is greater (see Fig. 1). The US economy therefore appears to be less at risk of a recession than the European economy, for example.

However, not everything is running smoothly in the US. One weak point, for example, is the construction sector, where the trend has been on a downward path since Spring 2022. Building permits and housing starts, which have somewhat slipped again in recent months, are more than 20% below the level seen at the beginning of 2022. A second weak point is the manufacturing sector. Industrial production has barely budged over the past two years, and incoming orders do not yet show any sign of a sustained improvement. The “new orders” component of the ISM survey even shows a decline reaching contraction criteria for the last six months, to 46.1 (neutral: 50.0) in September.

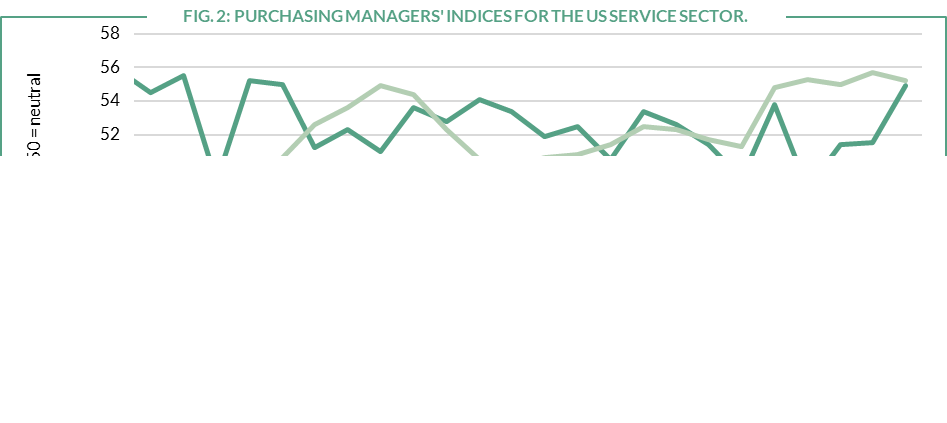

However, a further weakening in these areas is not likely to push the US economy into recession. These sectors’ overall economic weights are too low to be singlehandedly accountable: the construction sector (excluding real estate services) generated just under 4% of total economic output in the second quarter of 2020, while the manufacturing sector generated around 10%. By comparison, financial services alone accounted for more than 20%. Overall, most indicators point to a robust trend in the service sectors, which is far more central to the economy’s health. The purchasing managers’ indices for the service sector, both the ISM Survey and the S&P Global survey, show a level of around 55 for September (Fig. 2). In addition, the new orders indicator shot up steeply in September to 59.4. This is consistent with the employment trend, which picked up again in September. The service sector showed somewhat more volatility over the summer months, but the available data do not suggest any significant weakening.

Accounting for almost 70% of gross domestic product (GDP), it is above all consumption that determines the ups and downs of the US economy on the demand side. In the second quarter, private consumption rose sharply by 2.8% (quarter-on-quarter, extrapolated to an annual rate). For the third quarter at least, the result could remain similarly good, as far as can be seen from the available figures on personal consumer spending. So far, there is little sign of consumer restraint.